Disclaimer: This material is not financial or investment advice; it is just for informational reasons. There are dangers involved with borrowing against Bitcoin, such as the market being unstable, the possibility of liquidation, and the loss of collateral. Crypto-backed loans make you responsible for paying them back, which might put more stress on your finances. Only use Bitcoin as collateral if you know all the hazards that come with it.

For a lot of members who have held Bitcoin for a long time, the debate has changed from whether BTC is worth retaining to how to get liquidity without losing exposure. Some people suggest borrowing against Bitcoin instead of selling it once the asset class matures. This method doesn't actually lower risk because it adds leverage, liquidation thresholds, and operational complexity. Instead, market volatility, custody arrangements, and collateral restrictions determine whether a bitcoin-backed loan makes finances more flexible or more risky.

This article explains how borrowing against Bitcoin works in practice, why some investors prefer it to selling, and which risks must be carefully evaluated before using BTC as collateral. The objective is not to promote borrowing, but to provide a structured analytical framework for informed decision-making. Readers are expected to conduct their own research and assess whether this approach aligns with their financial situation and risk tolerance.

What Borrowing Against Bitcoin Means

Borrowing against Bitcoin refers to the use of BTC as collateral to secure a loan without transferring ownership through a sale [1]. The Bitcoin remains associated with the borrower, but access to the asset is restricted for the duration of the loan.

From a functional perspective, the process involves pledging Bitcoin as collateral, receiving funds – typically in fiat currency or stablecoins, and maintaining the collateral position under predefined monitoring and liquidation conditions. Because bitcoin-backed loans are generally overcollateralized, the value of the deposited BTC must exceed the borrowed amount, creating a protective buffer for the lender [1] [6].

While this structure is designed to mitigate counterparty risk, it exposes borrowers to liquidation if the market moves sharply against their position. As a result, borrowing against Bitcoin should be approached as a leveraged financial instrument rather than a passive liquidity solution.

Why Some Investors Borrow Instead of Selling

For many Bitcoin holders, selling represents the most direct path to liquidity. However, selling also results in a permanent reduction of exposure to the asset, which may conflict with long-term investment theses.

Borrowing against Bitcoin is often considered by investors who wish to preserve exposure while addressing short-term liquidity requirements. This approach mirrors practices commonly observed in traditional finance, where investors borrow against appreciating assets such as equities or real estate instead of liquidating them outright [7].

Within the crypto market, however, this strategy operates under materially different conditions. Bitcoin’s volatility compresses reaction times, and liquidation mechanisms operate continuously. Consequently, while borrowing can offer flexibility, it also demands a higher level of risk awareness and ongoing position management.

Market data shows that crypto-collateralized lending remains an actively used liquidity mechanism across different market conditions, reflecting sustained demand for borrowing without selling long-term holdings [3].

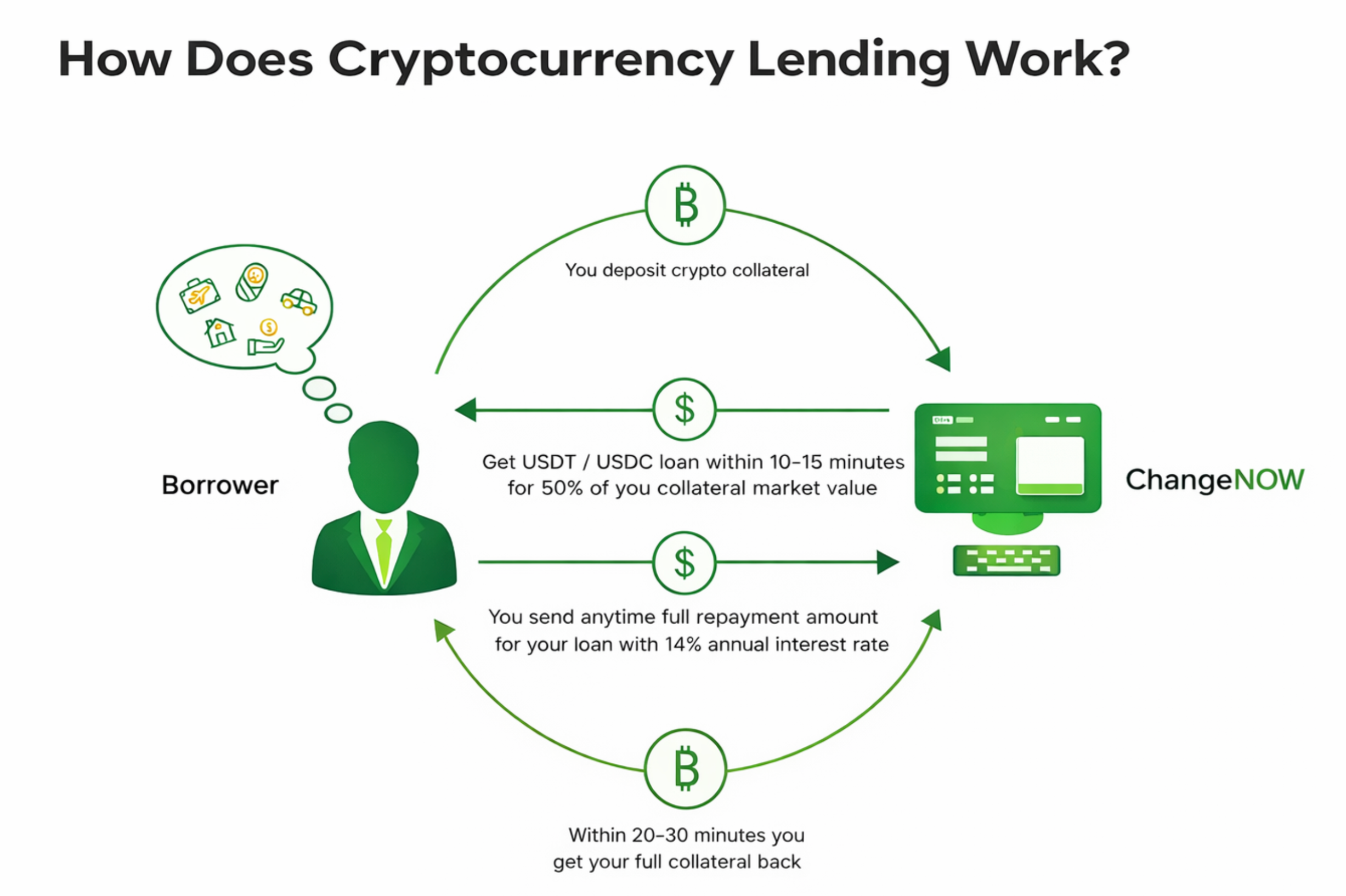

How Bitcoin-Backed Loans Work

Although implementation details vary across platforms and structures, Bitcoin-backed loans generally follow a consistent operational framework [5]. Bitcoin is first deposited as collateral, establishing borrowing capacity under a loan-to-value model. Loan parameters, including collateral ratios and liquidation thresholds, are defined in advance.

Once the loan is issued, the collateral is monitored in real time due to Bitcoin’s price volatility [5]. Repayment results in the release of the collateral, while failure to maintain required thresholds may trigger partial or full liquidation. This continuous monitoring model explains why borrowing against Bitcoin cannot be treated as a passive financial arrangement.

Before venturing further into the risk profile associated with Bitcoin-backed lending, it might be helpful to quickly describe how this tool of lending work. Although simple when broken down step by step, the cumulative effects associated with the process might be better understood when viewed as a whole.

Bitcoin-Backed Loans at a Glance

The table below provides a concise overview of the core characteristics of borrowing against Bitcoin, highlighting what remains under the borrower’s control, what becomes restricted during the loan period, and where the primary points of risk are concentrated [1] [6] [5].

Aspect

What It Means in Practice

Collateral

Bitcoin is locked for the duration of the loan and cannot be freely used

Ownership

BTC is not sold and remains associated with the borrower

Funds received

Fiat currency or stablecoins, not Bitcoin itself

Loan structure

Typically overcollateralized to protect against price swings

Monitoring

Collateral value is tracked continuously due to BTC volatility

Key risk

Liquidation if collateral value falls below required thresholds

User responsibility

Active position management is required

Suitable for

Experienced users with risk tolerance and liquidity buffers

Taken cumulatively, it becomes easy to understand why borrowing against Bitcoin can never truly be perceived as a strategy involving less work. Although the ownership over BTC is maintained in this process, the usage of the asset gets limited, and also it becomes prone to the effects of fluctuations in the marketplace.

This overview elucidates that the appropriateness of bitcoin-backed loans is contingent more upon a borrower's consistent risk management capabilities than on market optimism. With this basis established, it becomes simpler to analyze the particular dangers that arise when Bitcoin is utilized as collateral.

Centralized and Decentralized Borrowing Models

Borrowing against Bitcoin is typically facilitated through either centralized or decentralized lending models. While the underlying goal is the same–unlocking liquidity using BTC as collateral – the way risk is distributed across the system differs significantly between these two approaches.

The graphic image above delineates this divergence at a structural level. In centralized lending, the borrower interacts with a single institution that sits at the center of the process. This body assumes custody of the collateral, establishes lending conditions, oversees collateral conditions, and enacts liquidation if necessary. As a result, operational integrity, security practices, and solvency of the institution become critical factors. For users familiar with traditional financial intermediaries, this model may feel more intuitive, but it also concentrates custody and counterparty risk within one organization.

In decentralized lending, the structure displayed moves responsibility from middlemen to processes on the blockchain. Smart contracts take the place of custodians by enforcing collateral requirements, keeping track of price movements, and automatically starting liquidations when certain circumstances are met. This creates transparency and reduces reliance on the other party in the contract, although it also increases the burden on the debtor [5] [6].

When the two approaches are juxtaposed, the most important thing that is revealed is that neither a centralized nor a decentralized credit system is a risk eliminator. Centralized lending emphasizes institutional trust and operational safeguards, whereas decentralized lending emphasizes protocol design and user competency. Know each model's risk before borrowing against Bitcoin.

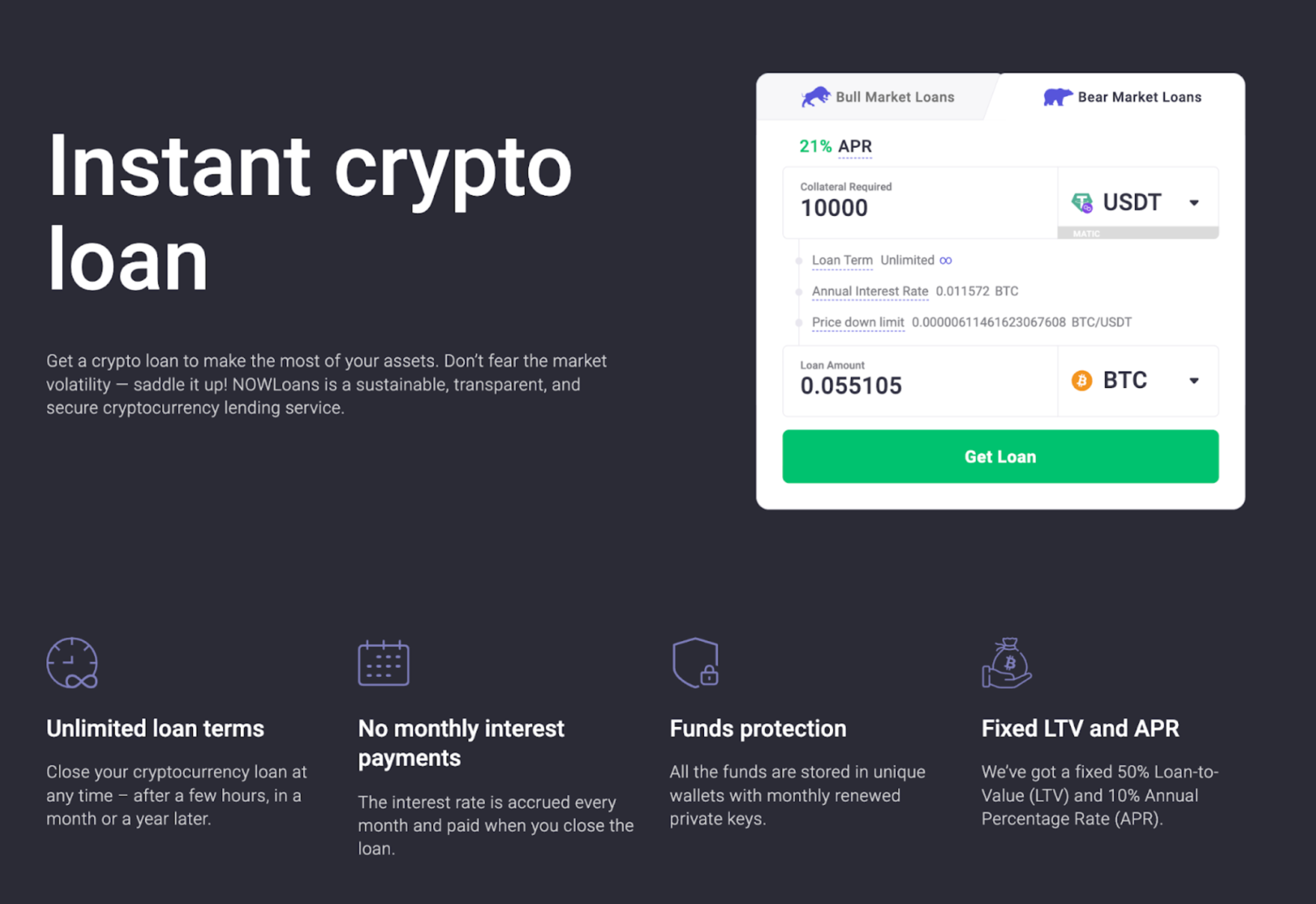

ChangeNOW Crypto Loans in Practice

ChangeNOW positions its bitcoin loan offering as a straightforward way to access liquidity rather than a product built around yield or financial engineering. The idea is to let users unlock capital while keeping their BTC exposure intact, without requiring them to navigate the technical and operational complexity that often comes with DeFi lending.

How this model works in practice:

Bitcoin is used as collateral without being sold.

Loan conditions are defined in advance and do not change mid-loan.

No interaction with smart contracts, oracles, or on-chain mechanics.

The level of the collateral ratio, or liquidation ratio, is clearly defined and disclosed initially.

Less need to continuously watch and adjust active position.

This structure does not eliminate risk, but it makes risk easier to understand and manage. Instead of shifting responsibility to protocol mechanics or constant user intervention, the emphasis is on predictability and operational simplicity. For users who want a bitcoin loan with clear rules and minimal overhead – rather than maximum flexibility or yield optimization – this approach offers a more controlled way to borrow against BTC.

Key Risks of Using Bitcoin as Collateral

Borrowing against Bitcoin inherently amplifies exposure to market dynamics. While the mechanics of collateralized loans may appear straightforward, the associated risks operate simultaneously and can compound during periods of market stress.

The primary risks include:

Liquidation risk

A decline in the value of Bitcoin collateral below predefined thresholds can trigger automated liquidation, potentially resulting in the partial or full loss of the pledged BTC [1] [5].

Market volatility

Bitcoin’s continuous trading and sensitivity to macroeconomic and market sentiment shifts can accelerate collateral deterioration, reducing the time available for corrective action.

Margin pressure

Sudden price movements may require borrowers to add collateral or reduce exposure on short notice, introducing operational stress during drawdowns.

Custody risk in centralized models

When borrowing through centralized structures, users are exposed to institutional risks related to custody, operational security, and liquidation execution.

Smart contract risk in decentralized models

In decentralized settings, flaws in protocol architecture, oracle dependencies, or execution logic might result in unforeseen consequences, irrespective of market direction.

Psychological pressure

Continuous monitoring, automated alerts, and rapid price fluctuations can impair judgment, increasing the likelihood of emotional or delayed decision-making at critical moments [7].

Laws and rules that apply in your area

Users are in charge of making sure they follow the rules and that they are eligible. Most lending platforms restrict access to users aged 18 and above. In practice, using Bitcoin as collateral demands ongoing attention, risk discipline, and an understanding of how the lending structure behaves under stress – not assumptions about where the price might go next.

Therefore, these risks explain why borrowing against Bitcoin requires active management and a clear understanding of both market behavior and structural mechanics, rather than reliance on price expectations alone.

Who This Strategy May Be Suitable For

For experienced traders who know how to use leveraged positions, have enough liquidity buffers, and are willing to actively manage collateral risk, borrowing against Bitcoin may be a good idea. For those who are having trouble with money, don't know much about collateralized lending, or need to borrow money to pay for basic needs, the method is usually not a good fit for their risk profile.

Risk Management While Borrowing Against BTC

While risk cannot be reduced totally, it can be mitigated through conservative collateral usage, partial exposure management, and continuous monitoring. For volatility, defining responses ahead of time diminishes emotional decision-making and enhances the possibility for controlled outcomes.

In fact, loans backed by BTC are usually given out right after the network confirms the collateral and released when the loan is paid back.

Each loan operates around a predefined liquidation price, which determines when collateral may be liquidated if market conditions deteriorate. Because loans can usually be closed at any time and managed independently, effective risk management depends on conservative collateral usage, continuous monitoring, and the ability to react quickly to changing market conditions [8].

Borrowing against Bitcoin requires more than choosing the right lending model. In addition, it is based on the efficiency of collateral, liquidity, and swift moves that do not incur custody risks in the process.

Non-custodial infrastructure may also play a crucial role if you are studying the topic of borrowing strategies and stablecoins as part of a risk management system. With the ability to exchange cryptocurrency assets using ChangeNOW, you can decrease the operational complexity associated with managing positions.

Asset execution separation tools may assist borrowers in having more control over the process of borrowing. This can be achieved through tools that separate asset execution from the logic of lending.

Borrowing against Bitcoin is a complicated way to get cash, not a one-size-fits-all way to do it. It lets holders get cash without selling BTC, which keeps them exposed to the market in the long term but also adds risks related to leverage, volatility, and managing collateral.

In practice, bitcoin-backed loans require a clear understanding of liquidation mechanics, custody models, and behavioral pressures that intensify during market stress [1] [5]. Because collateral enforcement is automated and pricing is continuous, outcomes depend as much on discipline and preparation as on market conditions.

For experienced investors who can handle some risk and have some cash on hand, borrowing against Bitcoin might be a useful aspect of a larger investment strategy. For some people, especially those who want to be sure or are under short-term financial stress, the dangers may be greater than the rewards.

In the end, this method is best thought of as a planned, well-informed choice. When borrowing is part of long-term plans, the infrastructure around it becomes quite important. Secure custody, transparent asset management, and tools that reduce operational complexity – such as professional environments like ChangeNOW Pro – can better support disc iplined risk management and long-term asset protection.

You start with Bitcoin. It gets locked. That’s the condition. How much you can borrow depends on price and limits set by the lender. Funds come later – usually fiat or stablecoins. If the loan is closed cleanly, BTC becomes accessible again.

There isn’t one place. Some loans come from centralized companies. Others run on-chain. The difference shows up when things go wrong – custody, liquidations, control. That’s usually where the “best” option becomes obvious.

Sometimes fast. As soon as the deposit is confirmed. Sometimes slower – internal checks, manual steps. It's not Bitcoin itself that matters; it's how the system is set up.

There is no universal answer. A good loan is one you can live with when the market moves against you. Clear rules matter more than attractive numbers.

No. If BTC isn’t locked, it’s not a bitcoin-backed loan. Everything else is just credit with a different label.

You send BTC in. You accept the terms. You receive funds. From that moment, the Bitcoin is restricted until the loan ends – one way or another.

What Is a Blockchain Explorer and How to Use It: Complete Guide 2026

Learn how blockchain explorers work and why they matter | Discover how to track crypto transactions, analyze wallet activity, and access network data with ease

What Is the Blockchain Trilemma? A Simple Explanation Everyone Can Understand

The blockchain trilemma explains why you can't have security, speed, and decentralization simultaneously. Learn why networks struggle to balance all three.

How to Get a Bitcoin Loan Without Selling BTC | Bitcoin Loans Guide | ChangeNOW Blog