Limit orders are a classic price-control tool. In traditional markets, they work predictably: users trade execution certainty for price certainty in environments with deep liquidity and stable rules.

In crypto, this assumption often fails. High volatility, fragmented liquidity, and non-standard execution models mean that reaching a price does not guarantee execution.

Most educational material stops at definitions. This article goes further. It explains what limit orders are, how they actually execute in crypto environments, and where Web3 fundamentally breaks the classical model. The focus is not on trading strategies but on execution mechanics and real-world behavior.

A limit order lets a trader decide in advance the price at which they are prepared to buy or sell an asset [1]. In a buy order, this sets the maximum acceptable price. In a sell order, it establishes the minimum price the trader is willing to receive. The order executes only if the market reaches the defined price level.

In simple terms, a limit order answers one question: at what price are you willing to trade?

Limit order price intent shown against market price movement.Reaching the price does not guarantee execution.

If the market reaches that price and sufficient liquidity is available, the order executes. If not, the order remains open or expires unfilled. This makes limit orders fundamentally different from market orders, which prioritize execution regardless of price.

Unlike market orders, which prioritize immediacy, limit orders prioritize price control. This distinction is often misunderstood. A limit order expresses intent under specific conditions, not a guarantee of execution.

In both traditional and crypto markets, limit orders help reveal where market participants are actually willing to trade. Whether that intent turns into a completed transaction depends on how the market is structured and how much liquidity is available at that price.

This mechanism assumes continuous liquidity. Crypto rarely provides it.

How Limit Orders Work in Practice

In most trading environments, limit orders operate within an order book, a structured list of buy and sell orders organized by price [4]. Buy orders populate the bid side, sell orders populate the ask side. Matching typically follows price-time priority: better prices execute first, and earlier orders take precedence when prices are equal.

At a mechanical level, a limit order works as follows:

The user specifies an asset, amount, and target price

The order is placed into the order book (or stored as a conditional instruction, depending on the platform)

The order becomes eligible for execution only at the specified price or better

Execution occurs only if sufficient opposing liquidity is available at that price

Any unfilled portion remains open until filled, canceled, or expired

In crypto markets, execution outcomes are heavily influenced by liquidity depth and timing.

Consider a simple example. A trader places a buy limit order for 1 BTC at $40,000. At that price level, the order book contains sell orders totaling only 0.4 BTC. In this case, the order is partially filled for 0.4 BTC. The remaining 0.6 BTC stays open, waiting for additional liquidity. If the market moves upward before more sellers appear at $40,000, the rest of the order is never executed.

Example of an order book showing bid and ask liquidity across price levels. Limit order execution depends on available depth, not price alone.

In periods of rapid price movement, a limit order at $40,000 may never fill, even if the market briefly trades through that level. Execution hinges on the presence of liquidity at that price at the precise moment it becomes available.

A Common Limit Order Failure Scenario

You place a buy limit at $40,000

The market touches $40,000 briefly and reverses

No execution occurs

Reason:

insufficient sell-side liquidity at that level

existing orders ahead of you absorb available depth

price movement happens faster than matching

Price touching a level does not create execution. Liquidity does. This is a critical difference from how many users intuitively understand limit orders. In crypto markets, touching a price level does not imply that sufficient liquidity exists to fill the order.

In real conditions, this often leads to missed execution. Reaching a price does not guarantee that the order will be filled, especially when monitoring depends on manual timing.

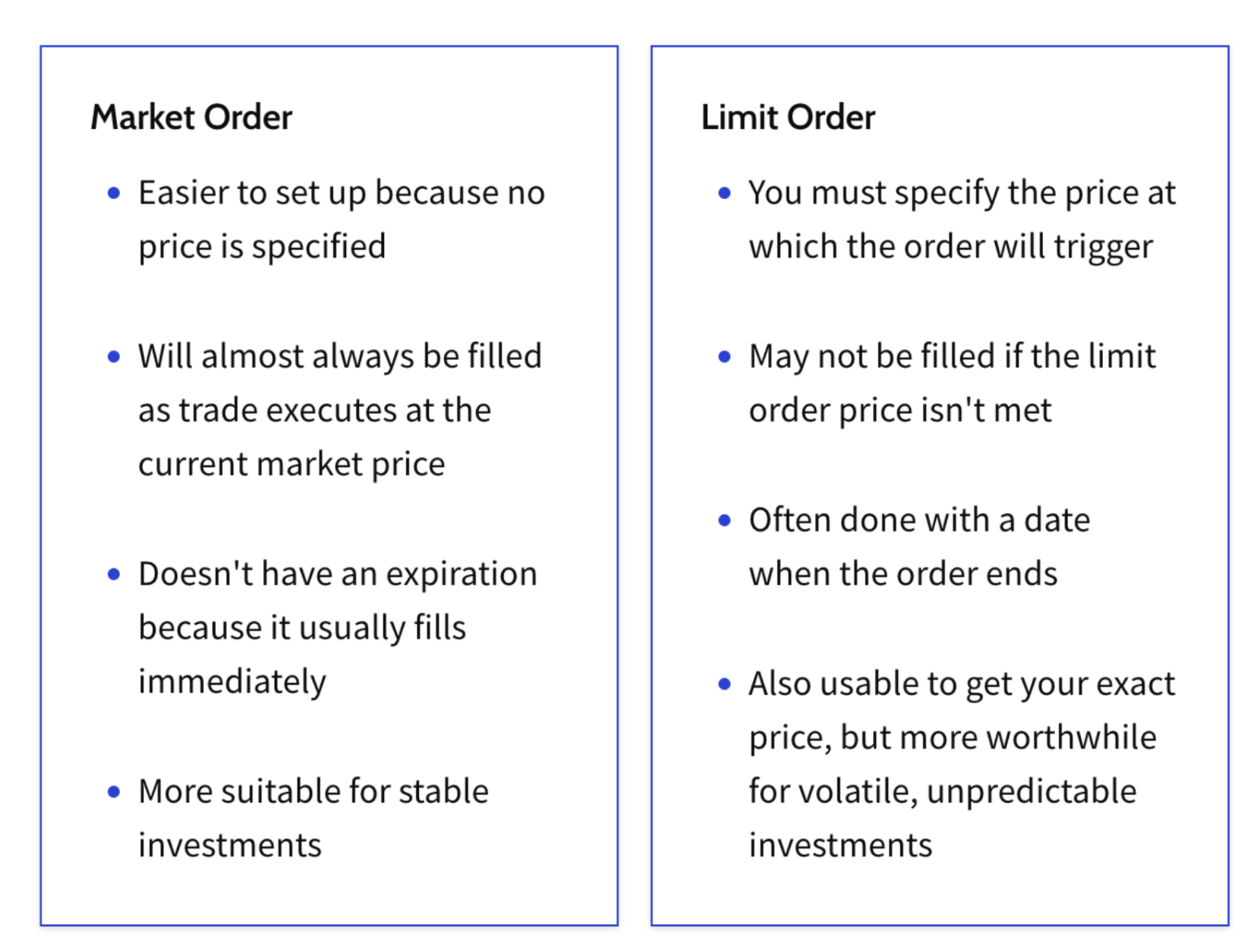

Limit orders and market orders prioritize different aspects of execution.

The contrast between price control and execution certainty becomes especially clear in volatile crypto markets.

Market orders are designed to execute immediately at the prevailing market price. Limit orders, by contrast, execute only under predefined price conditions and may remain unfilled if those conditions are not met [5].

Market orders focus on immediate execution, while limit orders focus on price control and may remain unfilled.

Aspect

Limit Order

Market Order

Price control

Explicit and predefined

None

Execution certainty

Conditional

Immediate

Slippage exposure

Low if executed

Potentially high

Liquidity interaction

Depends on depth at price level

Consumes available liquidity

Typical crypto use case

Planned entry or exit at a target price

Urgent execution during fast moves

In practice, market orders guarantee execution but may fill across multiple price levels, especially during sharp moves. Limit orders keep price under control but can remain unfilled. Market orders remove that risk at the cost of price certainty. Each fits a different execution intent.

When a Limit Order Is the Wrong Tool

A limit order is the wrong choice when execution matters more than price.

Typical cases:

fast market moves or breakouts

low or fragmented liquidity at the target price

situations where missing the trade is worse than small slippage

If participation is the goal, a limit order adds execution risk instead of reducing it.

Limit Orders Compared to Stop and Stop-Limit Orders

Limit orders are frequently confused with stop-based orders, particularly by users transitioning from traditional markets into crypto.

The difference lies in how execution is triggered.

Limit orders define execution conditions upfront. Stop orders define when execution begins. Stop-limit orders combine both, but remain dependent on post-trigger liquidity.

A stop order activates when the market reaches a specified trigger price, after which it converts into a market order. The trigger price is controlled, but the execution price is not. In fast-moving markets, this can result in significant slippage.

A stop-limit order adds a second condition. Once the stop price is reached, a limit order is placed instead of a market order. This restores price control but reintroduces the possibility of non-execution if liquidity is insufficient after the trigger.

The differences become clearer when comparing how each order type triggers execution and interacts with liquidity.

Aspect

Limit Order

Stop Order

Stop-Limit Order

Trigger

Price level

Trigger price

Trigger price

Execution type

Conditional

Market

Limit

Price control

Yes

No

Yes

Execution certainty

Conditional

High, (price not guaranteed)

Conditional

Common risk

Non-execution

Slippage

Non-execution after trigger

The distinction lies in sequence. Limit orders define execution conditions upfront. Stop orders define when execution begins. Stop-limit orders define both, but execution remains dependent on post-trigger liquidity.

In practice, stop and stop-limit orders are not protective variants of limit orders. They solve a different problem: timing, not price optimization. Misunderstanding this distinction often leads to unexpected execution outcomes in fast-moving markets.

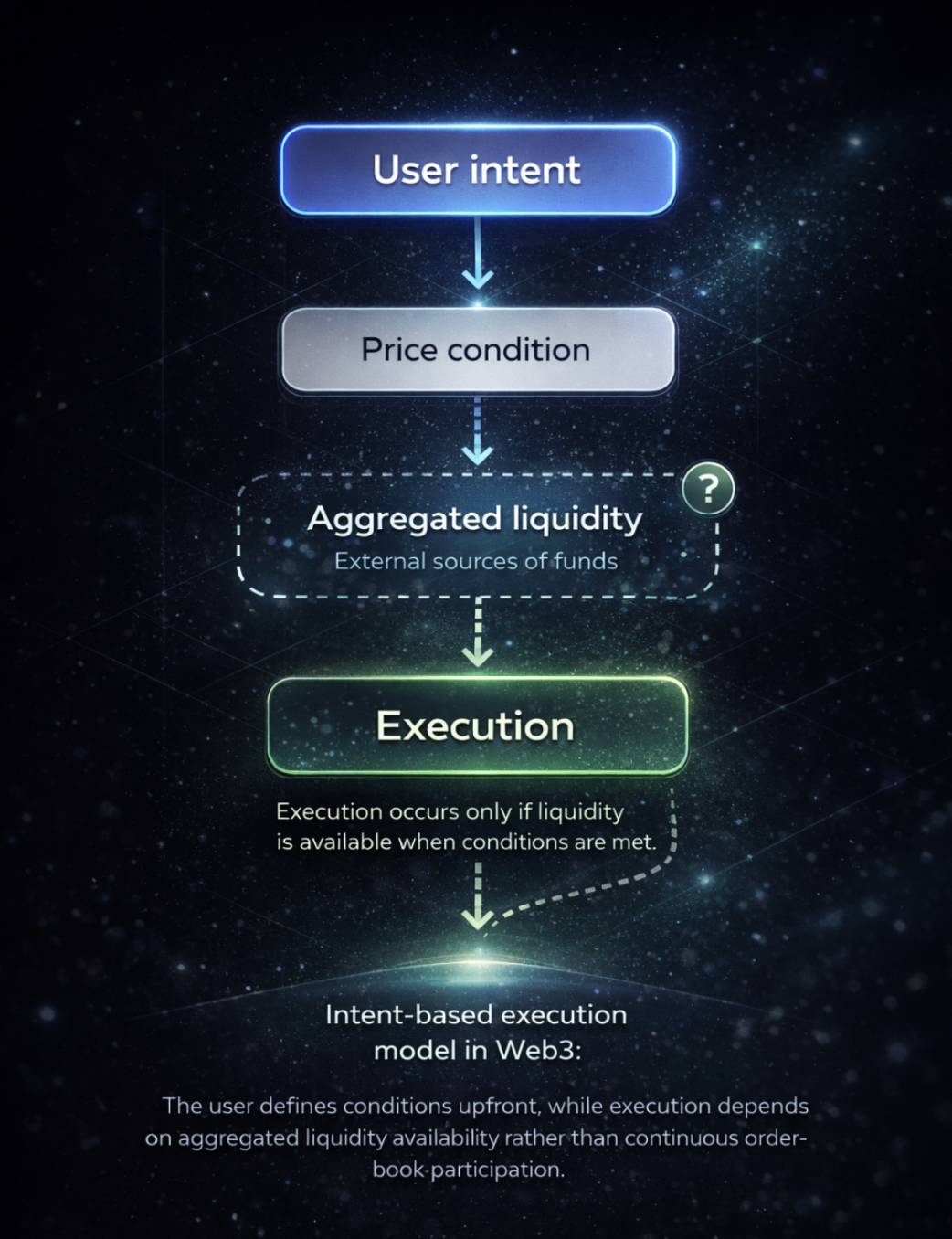

How Web3 Breaks the Classical Limit Order Model

Traditional limit orders rely on continuous order-book participation. Execution-first Web3 models do not. Calling both of these mechanisms “limit orders” obscures more than it explains.

What “Limit Order” Means in Execution-First Web3 Models

In execution-first Web3 systems, a limit order is not an order-book position.

no standing order in the book

no queue or price-time priority

no continuous market presence

Instead, the user submits an execution condition:

exchange only if external liquidity satisfies the target price

If liquidity never appears, nothing executes. This is intent-based execution, not market participation.

In execution-first environments, limit orders are implemented as conditional instructions rather than standing order-book positions. Execution occurs only when predefined conditions are met.

Execution-focused platforms such as ChangeNOW illustrate this shift [6]. ChangeNOW also supports limit orders in the Android app. Users can set target prices and manage active orders from mobile.

In these models, a limit order functions as a balance-to-balance exchange request that executes only when the target price becomes available through aggregated liquidity. The user does not interact with an order book, and the order does not influence market depth until execution occurs.

This model reflects a broader shift in Web3 toward intent-based execution rather than continuous market participation. The emphasis moves from managing open positions to defining precise execution conditions.

In this context, users are not managing open positions or market presence. They are defining execution intent and waiting for the market to satisfy it.

At the same time, this approach introduces clear boundaries. This execution model trades continuous market presence for conditional fulfillment. It does not support high-frequency or order-book-dependent strategies, and execution is entirely contingent on external liquidity becoming available.

Strategic Insight: The shift from order-book participation to intent-based execution changes user responsibility. Instead of managing open positions and market presence, users define execution conditions upfront and accept that fulfillment depends on external liquidity rather than continuous market matching.

Common and Costly Mistakes With Limit Orders in Crypto

Limit orders are often treated as passive safety tools, which leads to systematic errors.

One of the most common and costly mistakes is expecting guaranteed execution once a price level is reached. In crypto markets, price movement alone is insufficient; execution depends on available liquidity at that level.

Another frequent error is ignoring order book depth. A limit order placed at an illiquid price may execute only partially or not at all, even if the price appears favorable.

A third issue is applying traditional market assumptions without accounting for execution context. Assuming that limit orders are always safer than market orders overlooks a common outcome in fast markets: missed entries and partial fills.

The issue is rarely the order type itself, but how its execution behaves in a given environment.

Critical Warning: Treating limit orders as a safety mechanism is a category error. They reduce price uncertainty, not execution risk. In volatile or fragmented crypto markets, a limit order can fail silently – leaving users unfilled, exposed, or misaligned with market reality.

Conclusion

Limit orders remain a foundational execution tool, but their behavior in crypto and Web3 cannot be understood through traditional finance frameworks alone. Execution depends not only on price, but on liquidity structure, market design, and the underlying execution model.

For users, this means that understanding execution context is often more important than understanding order types themselves.

No. Limit orders execute only if sufficient liquidity exists at the specified price. In volatile or thin markets, orders may remain unfilled even if the price briefly crosses the limit.

No. Limit orders reduce price uncertainty but increase execution uncertainty. Their suitability depends on whether price control or immediacy is the primary concern.

Yes. In some Web3 models, limit orders function as conditional execution instructions rather than continuous order-book positions, which changes both their behavior and their limitations.

As conditional execution requests, not active market positions. No liquidity means no execution.

Because execution depends on available liquidity, not on price movement alone. If there is no depth at that level, no trade occurs.

What Is the Blockchain Trilemma? A Simple Explanation Everyone Can Understand

The blockchain trilemma explains why you can't have security, speed, and decentralization simultaneously. Learn why networks struggle to balance all three.

Start your journey into the realm of cryptocurrencies with this guide! The world of digital currencies like Bitcoin and Ethereum can seem daunting to newcomers. This beginner-friendly guide, brought to you by ChangeNOW, will help you understand the basics of cryptocurrencies and blockchain technology, and guide you through the simple process of crypto exchange. Get ready to explore the intriguing universe of digital currencies!