Blockchain vs Bank Transfer Fees 2025: Ultimate Cost Analysis

Sending $500 from the US to Europe? Traditional banks will charge $50–85 in fees, while blockchain can complete the same transfer for as little as $0.10. This hypothetical scenario isn’t speculation—it’s the financial reality of 2025. Our data-driven analysis shows when traditional banks still make sense and where blockchain offers significant savings.

Sending $500 from the US to Europe? Traditional banks will charge $50–85 in fees, while blockchain can complete the same transfer for as little as $0.10. This hypothetical scenario isn’t speculation—it’s the financial reality of 2025. Our data-driven analysis shows when traditional banks still make sense and where blockchain offers significant savings.

Key Takeaways

When sending $500 to another country, banks charge $50 to $85: Blockchain can do it for about ten cents, and you keep almost all of your assets.

Hidden Fees Are the Main Culprit: The biggest bank cost isn't the fixed fee but the 1-4% hidden FX margin, a cost eliminated by transparent, margin-free stablecoins.

Choose by Use Case: Use blockchain for speed and savings on most personal and business transfers (<$5,000). Use banks for large, regulated transactions where their insurance and consumer protection are worth the premium.

Deconstructing the Costs: Two Opposing Philosophies

The Traditional Bank Transfer: A Tax on Intermediation

A bank transfer's cost usually includes multiple items. It’s a sum of layered charges from a legacy system built on intermediaries [1]:

- Fixed Sender Fees: $15–50 for outgoing international wires [2]

- Correspondent Bank Charges: $10–30 per intermediary, unpredictable [3]

- Hidden FX Margin: 1–4% worse than interbank rate [4]

- Receiver Fees: Often deducted upon arrival [4]

The Blockchain Fee: Paying for Network Security

Blockchain fees are clear payments made for computational energy and network security.

- Network Fee (“Gas”): Variable, based on supply and demand [5].

- Disintermediation: No correspondent bank fees [5].

- FX Transparency: Stablecoins (USDC, USDT) eliminate hidden margins. The $180B+ stablecoin market cap ensures deep liquidity for reliable transfers [11].

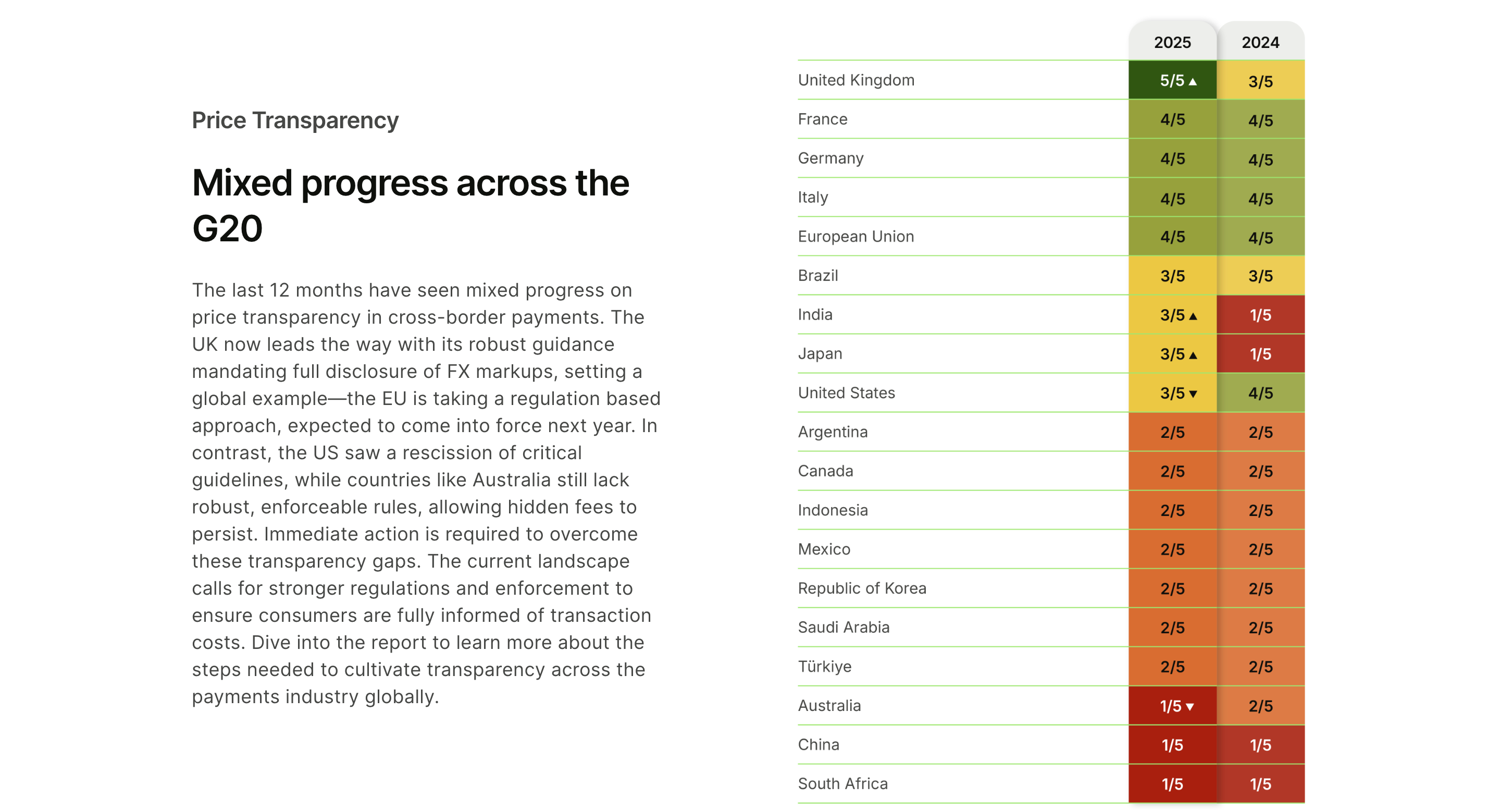

As the G20 transparency ranking shows, the core issue of hidden fees and inflated FX spreads persists in most major economies, including the regressing United States (3/5) and Australia (1/5). This regulatory gap is precisely what makes blockchain solutions so critical. Unlike the opaque traditional system, stablecoin transfers (e.g., USDC on Solana) provide the total, final cost upfront, technically eliminating the possibility of hidden markups. While the world debates transparency rules, blockchain delivers a functional technical solution today [4].

The Limitations of Blockchain: Insights Beyond the Headlines

- Volatility Exposure: Cryptocurrency values fluctuate 5–20% daily. Solution: use stablecoins [5].

- User Error Consequences: Wrong addresses lead to permanent loss (~$300M lost annually) [7].

- Regulatory Uncertainty: 45% of countries lack clear crypto regulations [5].

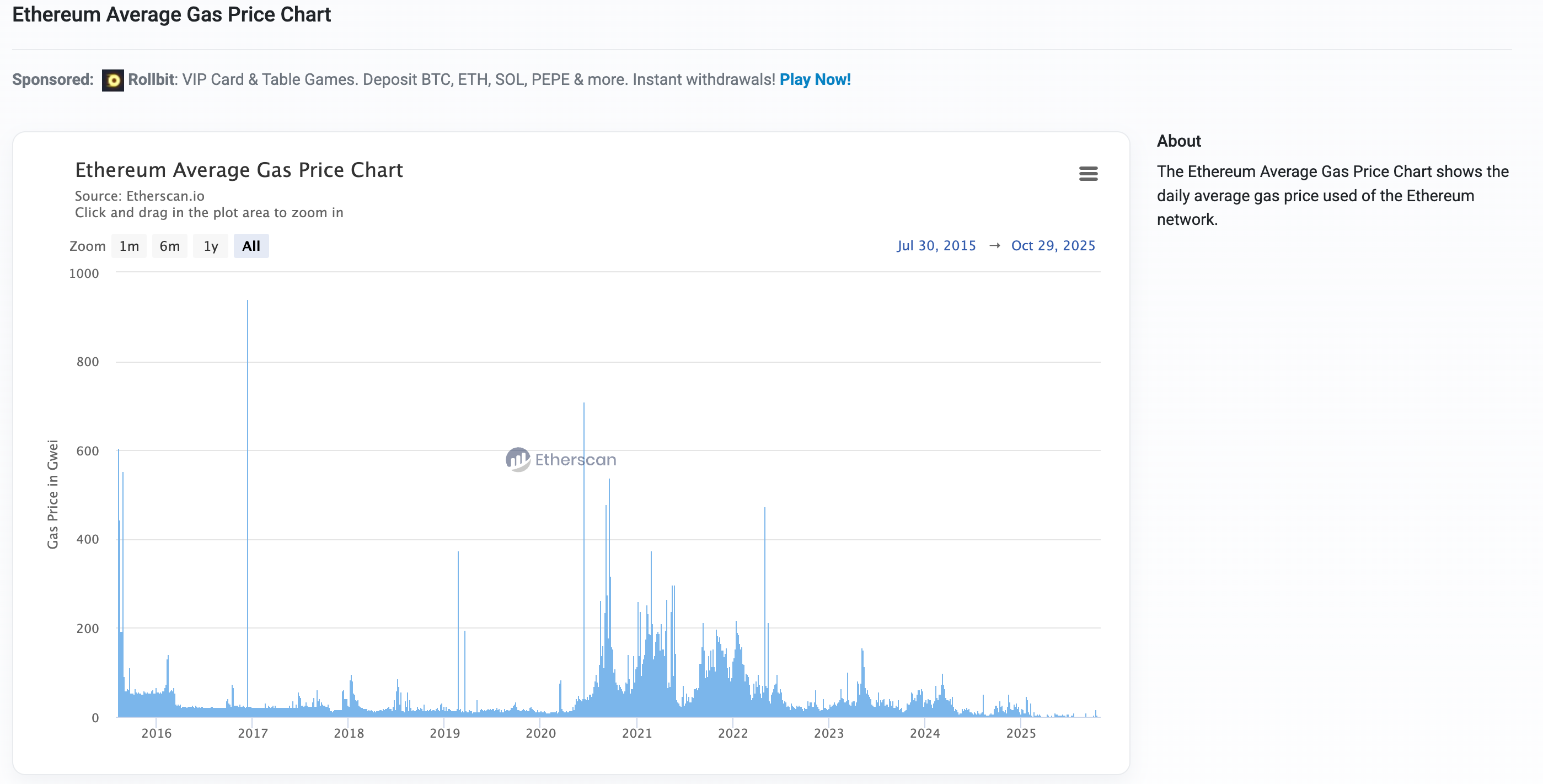

- Network Congestion: Ethereum fees can spike; Bitcoin may slow. Solution: Layer-2 solutions [5] [9].

The Rise of Layer-2 Scaling: The Lightning Network in Action

While volatility and congestion are real challenges on base layers like Bitcoin and Ethereum, scaling solutions are already live and solving these problems today.

Built on Bitcoin, the Lightning Network exemplifies a "Layer-2" protocol. It makes a network of instant, very low-cost payment channels that avoid the slower and more expensive main blockchain for small, frequent transactions.

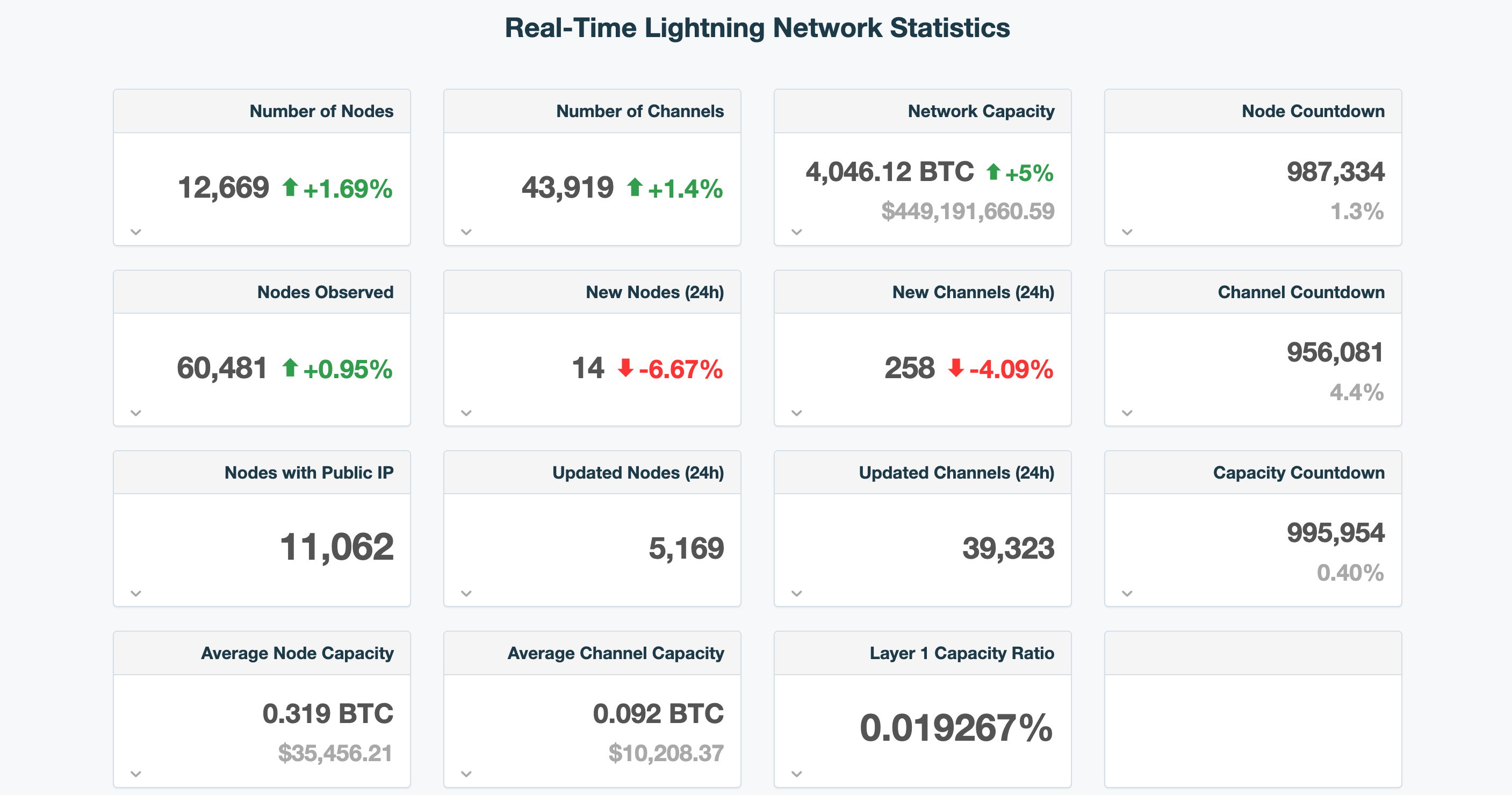

As the real-time data shows, this protocol isn't a niche experiment. With over 12,669 nodes, 43,919 channels, and a network capacity of over $449 million, the Lightning Network represents a massive, decentralized financial rail operating 24/7 [10].

This growth directly addresses the limitations of speed and cost, making blockchain payments feasible for everyday purchases and micro-transactions—a use case where traditional banking fees are most predatory.

The Data-Driven Showdown: Tables Don’t Lie

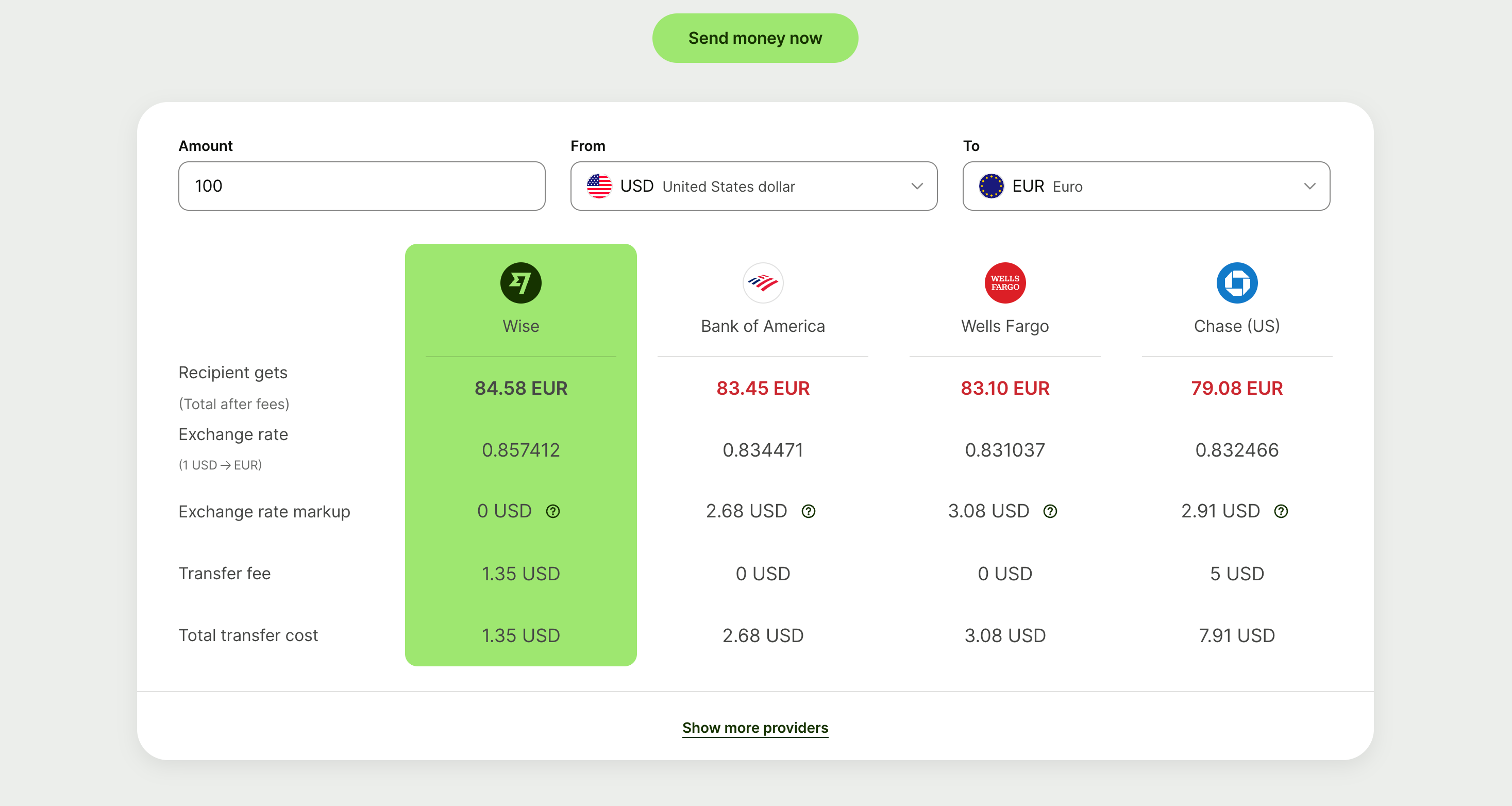

Fee Breakdown – Sending $500 from the USA to Europe

| Fee Component | Traditional Bank | Blockchain (Ethereum L1) | Blockchain (Solana/L2s) |

|---|---|---|---|

| Fixed Sender Fee | $25–45 [2] | N/A | N/A |

| Intermediary Bank Fees | $10–25 [2] | N/A | N/A |

| FX Margin (≈3%) | ~$15 [2] | ~$0 (Stablecoin) [5] | ~$0 (Stablecoin) [5] |

| Network Fee | N/A | $5–25 (Variable) [5] | $0.01–$0.10 [5] |

| Total Estimated Cost | $50–85 | $5–25 | ~$0.10 |

| Final Amount Received | $415–450 | $475–495 | $499.90 |

The "Sweet Spot" Analyzer—Which Option Offers Greater Cost Efficiency?

| Transaction Profile | Winner | Rationale |

|---|---|---|

| Micro-Transfer (<$100) | Blockchain (Solana/L2s) | The bank’s fixed fee can exceed 35%. Blockchain’s low fixed cost wins |

| Standard Transfer ($100–2K) | Blockchain (All Types) | Banks’ combined fees and FX margins are crippling. Blockchain saves big |

| Large Transfer (>$5K) | Competitive | The bank’s fixed fee becomes small, but hidden 3% FX margin on $5K = $150 |

| Speed-Critical Transfer | Blockchain | Banks: 1–5 days. Blockchain: minutes/seconds [6] |

Real-World Case Studies: The Challenges of Numbers

The theoretical savings from the table above are not just numbers—they are reflected in live network data and real-world payments.

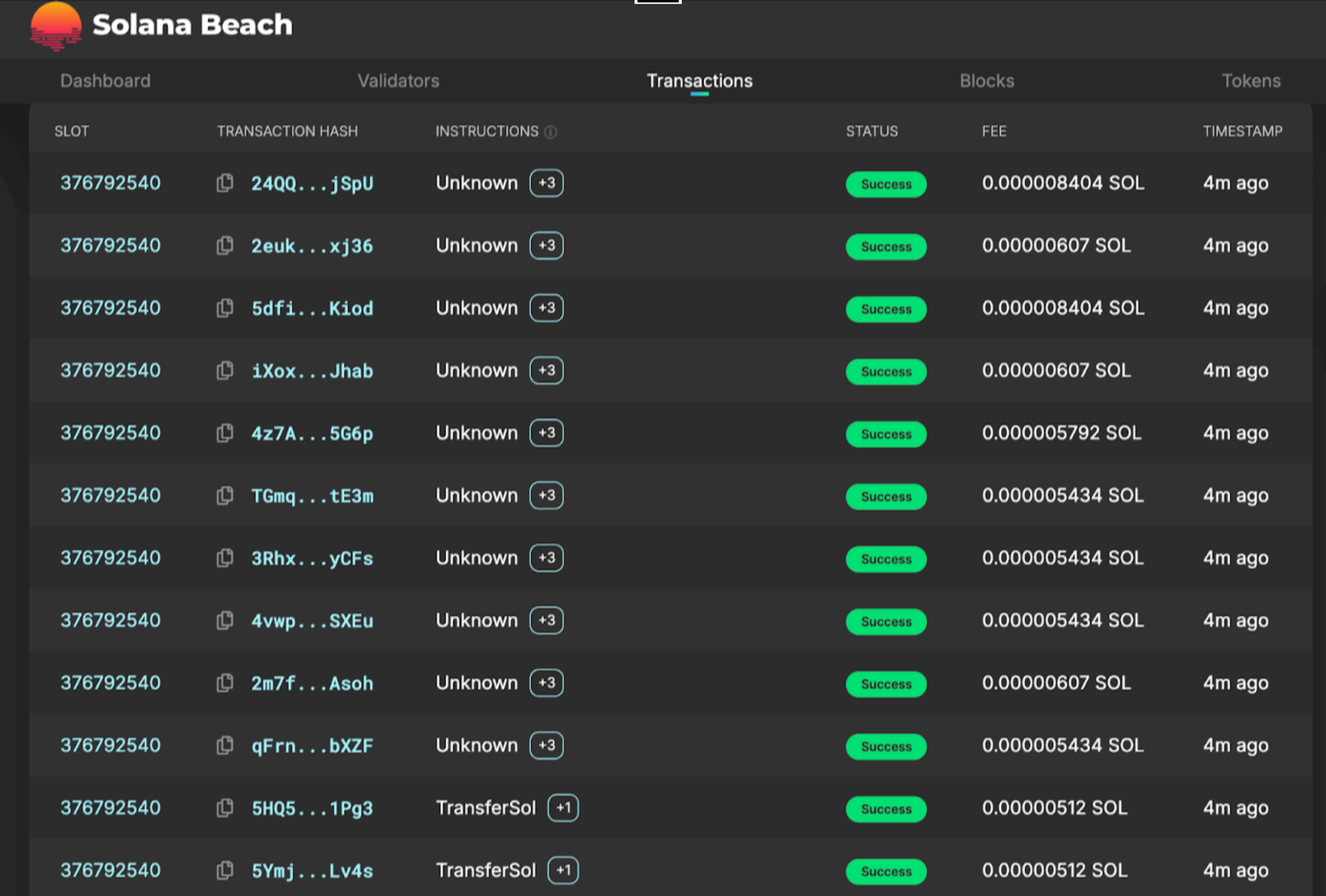

Live Network Proof: As data from the Solana Beach explorer confirms, the network processes transactions with fees consistently below $0.001 [14]. This microscopic cost base is the fundamental infrastructure that enables the dramatic savings in the following documented cases.

Documented Banking Fee Analysis

US → Europe Transfer:

- Bank FX Markup: ~$27.39 [4]

- Additional Fees: $15–25 fixed [4]

- Total Traditional Cost: ~$42–52 [4]

- Alternative Provider Cost: ~$9.87 [4]

- Savings: 76–81% [4]

Global Patterns:

- International Fees: $15–50 [7].

- Intermediary Charges: $10–30 [7].

- Small Business Impact: Companies spend $5–15K annually on fees [7].

Regional Case Studies

Southeast Asia – Freelancer Payments:

- Filipino developer receives $2,000 from US client

- Bank: 4 days, $145 total

- Blockchain: 12 minutes, $1.20 network fee via Polygon USDC [10]

- Savings: 99%

Latin America – Small Business:

- Brazilian exporter to Germany

- Bank: 5 days, $120 fees

- Blockchain: 2 hours, $0.45 via Solana USDC [12]

- Time Value: Funds 127 hours sooner

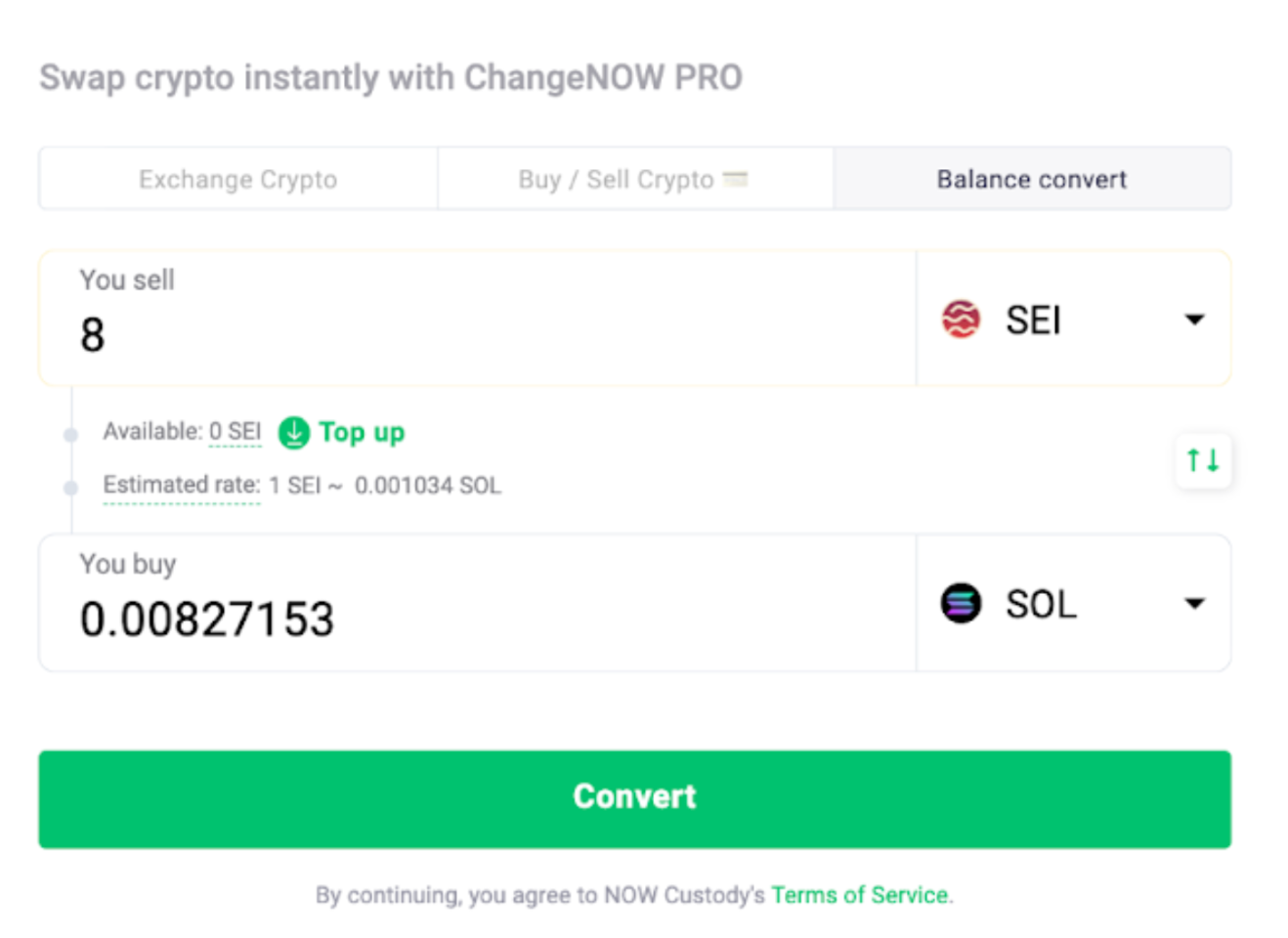

Learn how easy it is to convert Solana to Sei: it's just as simple as a bank transfer, but much faster and with lower fees! See the savings for yourself.

The Bottom Line: Where Blockchain Becomes Your Wallet's Best Friend

Let's cut to the chase. The theoretical advantage of blockchain becomes a tangible, hard-cash benefit in specific, everyday situations. The most dramatic savings appear where traditional banks are most inefficient: smaller amounts and urgent transfers.

Consider the classic US-to-Europe corridor. A Wise study [4] highlights that a standard bank transfer hides a ~$27 FX markup on top of fixed fees, bringing the total cost to over $50. For a small business paying a European freelancer $500, that's a 10% tax just on the payment mechanism. A blockchain transaction slashes this cost by over 80%, ensuring the freelancer gets the full value of their work.

This efficiency is even more critical in high-growth emerging markets. Let's take Turkey, where inflation has made the local currency volatile. A Turkish exporter receiving a €5,000 payment for goods can wait 3–5 days for a bank transfer and lose a significant portion due to devaluation and fees. By requesting payment in stablecoins, they receive the value in minutes, instantly converting only what they need to local currency. This isn't just about saving on fees; it's a powerful financial hedging tool.

The other undeniable advantage is radical transparency. With a bank, you often discover hidden correspondent bank fees and unfavorable exchange rates only after the fact. With blockchain, you see the total cost, every network fee included—before you confirm the transaction. No surprises, no "fee shock." This upfront honesty builds trust and allows for precise financial planning, a benefit both individuals and corporate treasuries are increasingly valuing.

At ChangeNOW, all the fees are already included in the calculator. Unlike bank transfers, ChangeNOW does not impose any hidden fees.

Security Comparison: Protection vs Control

| Security Aspect | Traditional Banks | Blockchain |

|---|---|---|

| Funds Insurance | FDIC/SIPC insured up to $250K [8] | No insurance, self-custody |

| Fraud Protection | Chargebacks & dispute resolution | Irreversible transactions |

| Account Access | Password recovery, support | Private key = only access |

| Regulatory Oversight | Strong consumer protection | Evolving framework |

| Transparency | Limited fee disclosure | Full transparency pre-transaction |

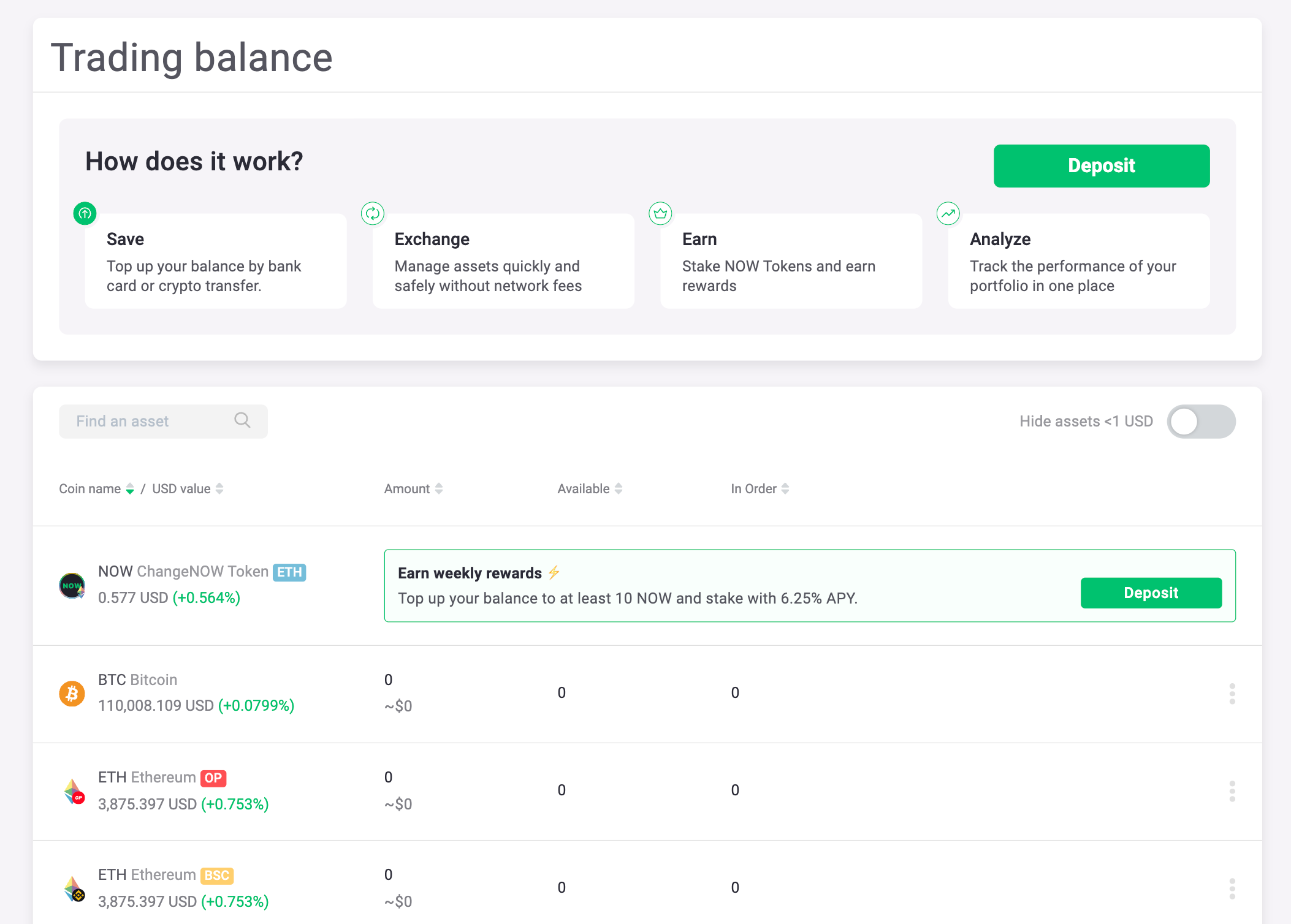

ChangeNOW Pro offers a custodial service that functions just like traditional bank transfers: easy, secure, and reliable. When you use our platform, we handle the transaction process for you, making it as seamless as a bank transfer, but with the added benefit of blockchain technology. All your transfers are fully secured, and the fixed fees are included upfront, ensuring no hidden costs.

This makes the process simple and trustworthy, with the security you would expect from a bank, but without the high fees and delays. You can exchange BTC for ETH (or any other supported cryptocurrencies) effortlessly, while we take care of the complexities.

Your 2025 Financial Playbook: Choosing the Right Tool

How do you handle this dual-system environment in 2025, keeping all of this in mind? Being strategic rather than dogmatic is crucial. Every system has a role, and the most astute users are those who are aware of which tool to use for which task.

Your Simple Guide:

- For speed and savings on most personal transfers, choose blockchain. Blockchain is your best option for payments under a few thousand dollars, whether you're sending money home, splitting expenses with a friend who lives overseas, or paying for an international service. Transparency, speed, and low cost are an unbeatable combination.

- For large, compliance-heavy transactions, traditional banks still have a role. When moving a down payment for a house or a large inheritance, the FDIC insurance, legal recourse, and regulatory oversight of banks can be worth the premium price and slower speed. The priority here shifts from cost-efficiency to risk mitigation.

- For accessing the world of digital assets, non-custodial exchanges are the essential bridge. Want to convert your crypto, explore DeFi tokens, or simply buy your first Bitcoin with a bank card? Platforms like ChangeNOW offer a seamless, secure, and instant gateway without the complexity of managing private keys, making the power of blockchain accessible to everyone.

Ultimately, the "better" system depends entirely on your goal. The 2025 financial landscape isn't about picking one over the other; it's about achieving financial fluency in both. Use blockchain for its efficiency and empowerment. Use banks for their stability and protection. By understanding the strengths of each, you don't just save money—you take full control of how you move value in a connected world.

Your First Blockchain Transfer: Step-by-Step

- Choose Your Platform: Non-custodial exchange (easiest) or wallet (more control)

- Select Stablecoins: Use USDC or USDT to avoid volatility

- Verify Addresses: Double-check the recipient's wallet address

- Test First: Send a small amount before a large transfer

- Track Transaction: Use blockchain explorers to monitor progress

- Confirm Receipt: Ensure funds arrive before completing business

Pro Tip: Start with transfers under $100 to build confidence in the process.

Conclusion

The ledger doesn’t lie. In 2025, blockchain will no longer be considered an "alternative"; it will be the rational choice for cost, speed, and transparency. Banks are still needed for big, regulated transactions, but decentralized networks can save you 70–90% on most international transfers.

As blockchain technology gets better and more people start using it, we are seeing a big change in how money moves between countries.

The blockchain revolution has made finance's future borderless, decentralized, and not tied to old systems.

FAQ: Your Blockchain Transfer Questions Answered

Is blockchain really less expensive for transfers under $100?

Yes, a lot. A bank's $15–30 fixed fee can take up 15–30% of a $100 transfer, but a blockchain transaction on networks like Solana costs less than $0.01 and keeps more than 99% of the value.

What is the single biggest risk when using blockchain?

User error. Sending funds to an incorrect wallet address results in permanent, irreversible loss. Always double-check addresses and perform a test transaction first.

How much are "gas fees" in reality?

They vary by network:

Ethereum (L1): $2-15 (normal activity) [5]

Solana / Polygon: $0.001 - $0.10

For regular transfers, using Layer-2s or networks like Solana is essential for low costs.

Are stablecoins like USDC safe to use?

Leading stablecoins like USDC are highly secure. USDC is issued by Circle, a regulated entity that holds its reserves in cash and short-term U.S. government bonds, with these reserves verified by independent monthly attestations [11].

What happens if I send crypto to the wrong address?

The funds are permanently lost. There is no bank support or chargeback mechanism. This situation underscores the critical need to verify addresses and conduct test sends.

How does blockchain compare to modern fintech (Wise/Revolut)?

Fintech apps save ~50–70% versus traditional banks. Blockchain saves 90-99% by disintermediating the entire system. The trade-off is fintech's simplicity versus blockchain's ultimate cost efficiency and user responsibility.

When should I still use a traditional bank?

For large, compliance-sensitive transactions (e.g., a house down payment). In these scenarios, the FDIC insurance and legal recourse justify the higher cost and slower speed, prioritizing risk mitigation over cost-efficiency.

References (2025)

- Bank for International Settlements - Cross-Border Payments 2025

- World Bank - Remittance Prices Worldwide 2025

- Federal Reserve - Payment Systems 2025

- G20 Cross-Border Payments: Transparency and Cost Efficiency Report 2025 – Wise

- Ethereum Average Gas Price Chart – Etherscan

- Swift Cross-Border Payment Report 2025

- Chainalysis Crypto Crime Report 2025

- FDIC Risk Review 2025

- Ethereum Gas Tracker 2025

- Lightning Network Statistics 2025

- Stablecoin Market Cap 2025

- ChangeNOW Official 2025

- Wise Fees and Pricing Study

- Solana Beach Network Explorer - Live Transaction Fees