Blockchain is the name given to the technology on which cryptocurrencies, like Bitcoin, are based. Essentially, a blockchain is a database or a ledger. However, unlike traditional databases, blockchains are distributed. This means that they don’t rely on a central authority to update the data they store. Anyone who satisfies the rules of the network supporting a particular blockchain can update the ledger. This enables blockchains to create trust between parties that wouldn’t necessarily trust one another. Everyone can trust the blockchain instead.

The most successful application of blockchain technology to date was its first. Despite never actually using the term itself, Bitcoin’s anonymous creator, Satoshi Nakamoto, introduced the concept of a blockchain to the world. In more than a decade since, Bitcoin has inspired many other potential use cases for blockchain technology, as well as the creation of plenty of other cryptocurrencies. While it’s still early days for the technology, no application to date has been as successful as Bitcoin.

Why is Blockchain so Important and Interesting?

Databases aren’t that exciting. You’ll be well aware of this if you’ve ever been tasked with updating one. Blockchains, on the other hand, are much more interesting. Their design allows for the storing of data in ways not previously possible with traditional databases. Their properties include:

Distributed, trusted data storage. Rather than rely on a central authority, blockchains are kept up to date by a distributed network of participants. This removes a lot of the trust requirement from a system, meaning distributed parties can cooperate through mutual trust of the blockchain itself.

Highly secure. Thanks to certain features of their design, data stored to a blockchain is incredibly difficult to change in a valid manner once it’s been recorded. This is very important for cryptocurrencies, as well as those using the technology in enterprise applications.

How Does a Blockchain Work? A Closer Look

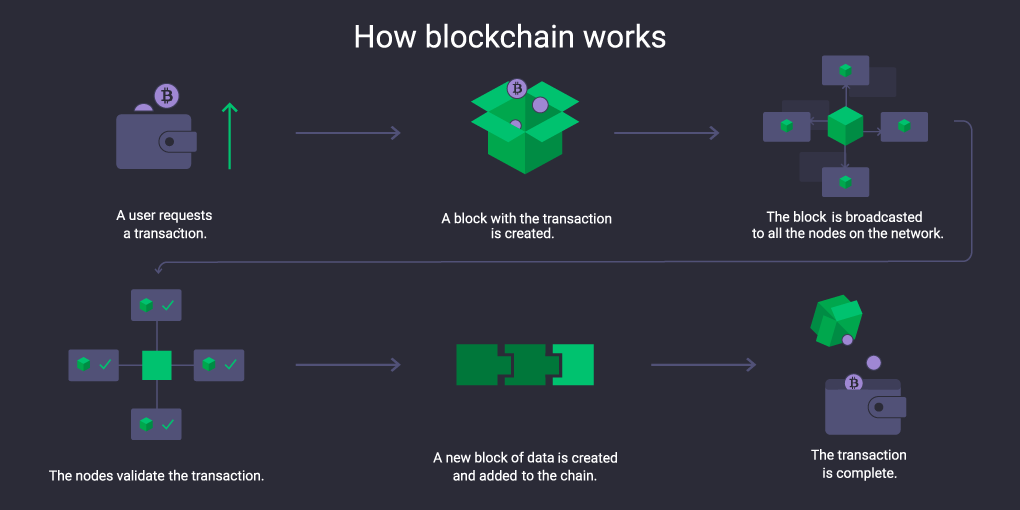

A blockchain is literally a chain of blocks. The block part refers to how new data is organized before it is recorded to our distributed database. Network participants group data into blocks. These blocks are then added to the ledger at regular intervals.

New blocks are shared with the rest of the network that either agrees or disagrees that the data contained follows the predetermined network rules. If the network agrees, the block is added and the network starts the process of adding another new block to the chain. If it disagrees, it rejects the block and starts trying to add a new block of data.

The blocks are “chained” together using a cryptographic function known as a hash. Basically, a hash is a way of representing a fingerprint of data as a string of letters and numbers. A hashing algorithm can represent a huge amount of data in a seemingly random looking collection of characters. Every hash is unique to the specific data hashed. Even a very small change to the data will produce a completely different hash.

Each block not only contains the transaction data to be recorded, but also the hash of the previous block’s data. This is important since it makes the data very difficult to change once added to the database. With each block referring back to the previous one, attempting to alter the data in a block that’s already been recorded changes the hash of that block. Since that hash forms part of the data in the next block, the hash of all subsequent blocks will be completely different, too. Adjusting the data in a specific block would, therefore, require changing every subsequent block, making cheating a blockchain system in any way incredibly resource intensive.

To ensure this level of security, blockchains rely on a mechanism called a consensus algorithm. This allows network participants to agree on the state of the database. It’s very important that the entire network agrees on the data recorded previously. If every participant was attempting to update a different database, the data would be different depending on which participant you asked. This would be chaotic and, ultimately, render the system entirely useless.

There are two main types of blockchains: public, or permissionless, blockchains and private, or permissioned, blockchains.

Public Blockchains

Public blockchains are distributed databases that are updated by a network that anyone can join and become a validator of data. Cryptocurrencies, like Bitcoin and Ethereum, are based on public blockchains.

Currencies rely on trust to be of any use. A monetary system would be a spectacular failure if those using it could change how much money everyone had or could spend the same units more than once. Satoshi Nakamoto, therefore, needed to find a way of ensuring that the record of transaction data could not be adjusted after it had been recorded. His solution drew on the work of many earlier cryptographers, combining concepts to create a system for recording transactions that was incredibly resistant to change. The distributed database of ordered blocks of data, eventually, became known as a blockchain.

Bitcoin and many other cryptocurrencies allow any individuals who want to participate in the system to do so. Participants, or nodes, just download the existing blockchain, as well as software to connect to the network. They can then start contributing. The software needed is free and completely open-source (anyone can review the code itself). No one can stop anyone else from joining the network and all the data recorded is publicly available for everyone to see.

So far, permissionless blockchains have provided the means to store data for cryptocurrencies like Bitcoin, Litecoin, and Monero. They’ve also been used to store other data relating to smart contracts. You can think of smart contracts as being like programmable money. For example, using a platform like Ethereum, EOS, or Tron, anyone can create a smart contract that will transfer money to a different address if some specified event occurs. This allows for the creation of decentralized applications for a range of uses. Among others, existing use cases of blockchain-based smart contracts include: lending, borrowing, insurance, and simple games. However, we’re only just starting to scratch the surface of the technology’s capabilities.

Private Blockchains

The second type of blockchain is a private or permissioned one. These are more useful for business applications. While the participants need to be approved by a central authority, their design is similar to public blockchains.

Rather than storing transactional data, as in the case of public blockchains, private blockchains are more likely to be used for proving the authenticity of an item or for recording ownership. One early use case for private blockchains, for example, is supply chain management.

A supermarket that works with a fishery could use a blockchain to keep a record of a specific fish’s journey from the sea to the shelves. The fishermen, any delivery companies used, the supermarket itself, and anyone else important to the item’s journey could all update the chain with data. Each step in the supply chain would be recorded by a different preapproved network participant. Obviously, it makes no sense for literally anyone to be able to participate in such a system. Only those involved in the actual supply chain process need permission to update the ledger.

Each fish could be electronically tagged and its date of catch, the temperature it had been kept at, and other important details relating to the quality of the end product could be recorded along the way. The customer could then scan a QR code and check that the item was absolutely fresh. The immutability of the blockchain would provide great confidence in the quality of the item being sold.

Like public blockchains, the practical uses of permissioned blockchains are still being explored. However, companies have already implemented them to track the authenticity of diamonds, the fairtrade claims of certain products, the ownership of a given item, and even voting.

Blockchain Technology Use Cases: A Revolution in Data Storage

Blockchain technology has only been around for as long as the Bitcoin network has existed. However, it’s already found quite a few interesting use cases. Thanks to its application in cryptocurrencies, many believe its invention has started fundamentally changing the way humans interact. Previously, it simply wouldn’t have been possible to send money from one side of the world to another without relying on a trusted central authority. Blockchain makes it possible.

Thanks to the constant efforts of those developing networks like Ethereum, public blockchains are starting to find even more novel applications. For example, the summer of 2020 saw an absolute explosion of interest in decentralised finance. Still an evolving sector, developments in the niche are already providing access to services to those previously excluded from the financial services industry.

Similarly, there is great enthusiasm for the future of permissioned blockchains. Thanks to their ability to record data in a transparent way that’s incredibly difficult to change, distributed ledger technology looks set to shakeup many industries. Companies spend big money attempting to ensure trust between themselves and customers and blockchain could dramatically reduce their operational costs by doing away with expensive auditing services.

Such innovation has occurred in just over a decade. In another ten years, it’s almost certain that blockchain will have found even more interesting use cases. By enabling trust where previously it was lacking, it’s fair to say that blockchain technology represents a real revolution in the way humans interact with one another and an exciting new chapter in the move towards greater digitisation of our world.

How to Buy Your First Crypto: Beginner’s Guide 2026

Crypto has a reputation for being complicated. With this complete beginner’s guide, you'll learn how to buy cryptocurrency in 2026. We'll cover all the basics you need to know: how to buy your first crypto, and how to keep it safe after.

With the NOT and USDt-TON listings, TON ecosystem attracts more and more crypto users. In this article, we'll dive into what Jettons are, how they work, and why they are gaining traction in the crypto community.