Headlines love a "flip." But a market-cap crossover between a blockchain and a dollar-pegged token isn't a contest with a winner. It's a prompt to ask what each asset is actually good for. This piece breaks that question down into six concrete use cases and looks at what actually drove the numbers together for a few hours in June 2026.

What Happened on June 26, and Why It Wasn't Luck

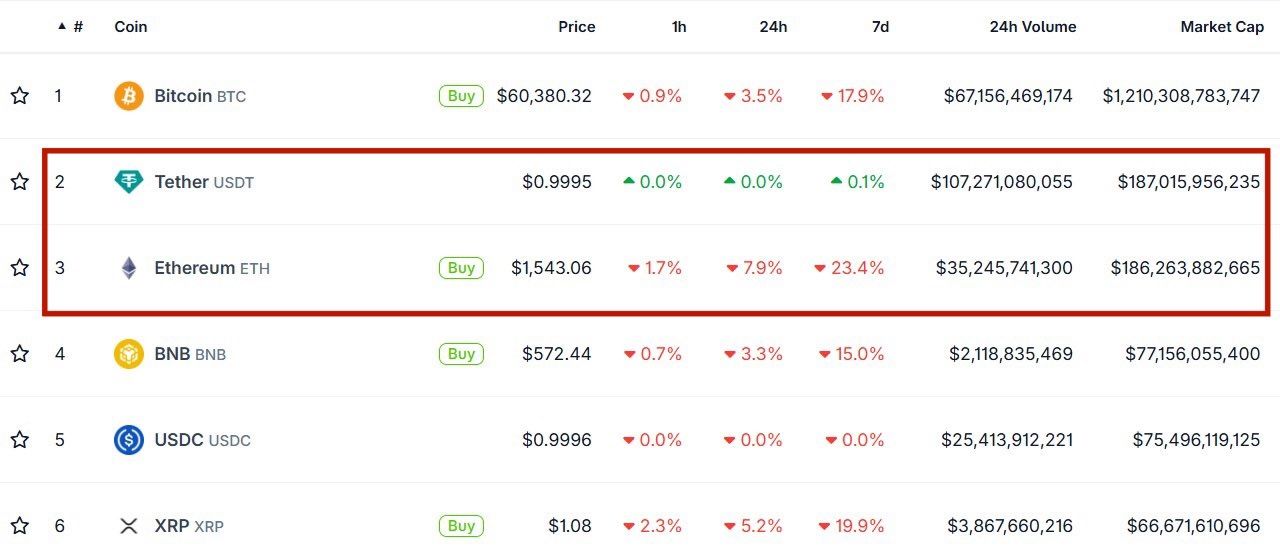

For a few hours on June 26, 2026, Tether briefly outranked Ethereum.

As ETH sold off into the $1,500–$1,600 range, lowest level of the year, Tether's USDT slipped into second place by market capitalization. The numbers were close: USDT at roughly $186.15 billion, ETH at roughly $185.263 billion. Ethereum clawed back the position within hours.

Three factors benefited Tether outperforming Ethereum in terms of market cap in June 2026:

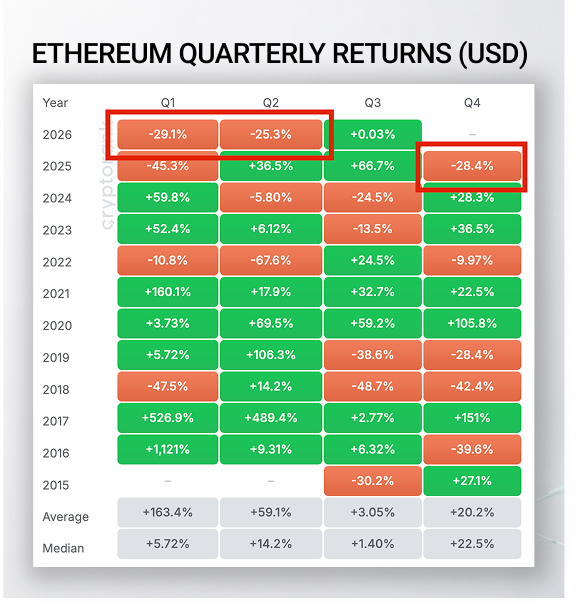

First, Ethereum was already in genuinely uncharted territory. According to CoinGlass data, ETH closed Q4 2025 down 28.2%, Q1 2026 down roughly 29%, and Q2 2026 down around 25%. That's three consecutive red quarters Ethereum has never done in its entire history.

Spot Ethereum ETFs logged their seventh straight week of net outflows heading into the June 26 event. The Ethereum Foundation had already cut its headcount by 20% and operating budget by 40%:

Second, dollar-denominated liquidity kept growing. Tether added $12.4 billion in USDT supply in Q4 2025. By Q1 2026, Tether's own attestation showed $1.04 billion in quarterly net profit and a record $8.23 billion capital buffer.

This wasn't just a Tether-specific issuance story, either. Total stablecoin dominance roughly doubled over the year, climbing from around 7.5% to an all-time high of 15.4%.

It happened in two distinct surges, and both line up almost exactly with Ethereum's worst stretches. The first, in late January and early February 2026, coincided with the start of ETH's 29% Q1 decline. The second, in the final weeks of June, coincided with the run-up to the June 26 flip itself.

Third, regulation actively reshapes the map, in opposite directions for each asset. We break down what's happening in more detail in the Regulation section below.

In short: the same week Tether was being formally pushed out of one major jurisdiction while Ethereum was being formally welcomed into another.

It's a good excuse to stop asking "which one flipped which" and start asking a more useful question: for six specific jobs an investor might actually need done, which asset does that job better?

Internal ChangeNOW data for the first half of 2026 backs up the picture painted above from the point of actual user activity.

Month-over-month transaction counts for ETH and USDT moved in a broadly synchronized wave from January through June: both dipped in February, then rebounded sharply in March and kept climbing into April.

The two diverged in May-June: USDT transaction volume held steady to slightly positive through this period, while ETH moved the opposite way, growing in May only to drop noticeably in June.

Notably, this divergence holds consistently across USDT's major networks. It reflects a genuine shift in user behavior rather than an artifact of a single chain.

In other words, in the month leading up to the June 26 flip, ChangeNOW users were already voting with their transactions for USDT over ETH. It's a sign the market-cap shift wasn't an isolated event, but part of a broader behavioral trend visible in actual exchange volume as well.

How We're Comparing Two Assets That Aren't Really Comparable

Before the scorecard, a disclosure: Ethereum and Tether are not the same type of asset, and any comparison that pretends otherwise is misleading by construction. So instead of a single verdict, this piece scores both assets across six concrete use cases.

How Tether and Ethereum Compare Across Six Real-World Use Cases

Use case

Verdict

Why

Store of value

Tether (technicality)

Holds $1 by design; but ETH's own scarcity thesis (net deflation) has quietly broken, while USDT offers no inflation protection either

Payments

Tether

$33T in 2025 stablecoin volume beat Visa+Mastercard combined; ETH isn't designed to be spent

Yield

Ethereum

~2.8–4% native staking yield vs. a legal ban on Tether paying holders any yield at all

Regulation

Ethereum

SEC/CFTC "digital commodity" status vs. Tether's EU delisting and GENIUS Act ineligibility

Institutions

Ethereum (as infrastructure)

BlackRock, JPMorgan building on it directly; Tether is a macro entity, not a platform others build on

Censorship resistance

Ethereum

No base-layer freeze mechanism, vs. Tether's active, disclosed freezing capability

1. Store of Value

Verdict: Tether by design, not by strength

On the narrowest possible reading, "does the number stay the same", Tether wins by design. USDT is redeemable at $1, that's the entire point of the asset.

But the more interesting story is what's happened to Ethereum's own scarcity thesis, because it's quietly broken.

The "ultrasound money" narrative hasn't played out as advertised.

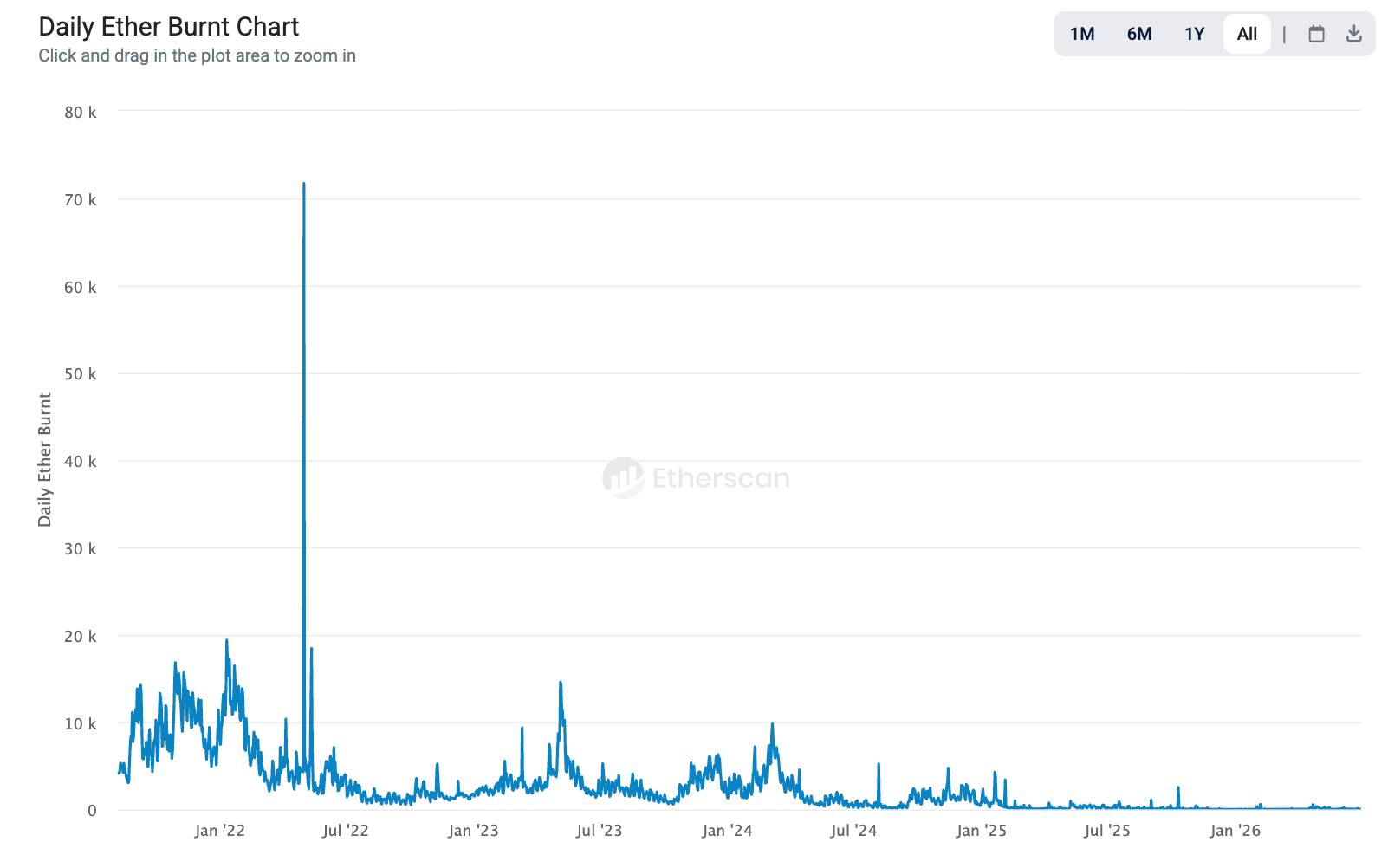

The 2024 Dencun upgrade pushed most Layer-2 activity off Ethereum's mainnet. That cut deep into the fees that used to get burned. Daily burns dropped from thousands of ETH in 2022 to just 50–70 ETH now, but stakers still get about 1,700 new ETH a day.

Result: Ethereum's supply has grown by about 950,000 ETH since the Merge, to roughly 121.5 million tokens. That's mild inflation (~0.23% a year), not the deflation Ethereum promised.

Meanwhile, Tether's "store of value" claim has its own asterisk: it stores nominal dollar value while doing nothing to protect purchasing power against dollar inflation. And, as covered in the Yield section below, US law now explicitly forbids Tether from compensating you for that erosion.

So the framing is: Tether is an excellent short-term capital-preservation instrument and a mediocre long-term store of value; Ethereum was supposed to be a long-term store of value with a shrinking supply, and for now that mechanism is dormant.

2. Payments

Verdict: Tether, clearly

This is the use case where the category mismatch matters most.

USDT runs on several chains, including Ethereum. For big institutional transfers and DeFi applications, Ethereum (plus its Layer-2s) still leads. But for everyday transfers Tron has become the go-to highway.

Stablecoins beat the traditional cross-border system, not just ETH. Stablecoins collectively processed roughly $33 trillion in on-chain transaction volume in 2025, outpacing Visa and Mastercard's ( $25.5 trillion). USDC led that figure with about $18.3 trillion (55%), and USDT followed with roughly $13.3 trillion (40%).

So the payments verdict really has two layers: Tether-the-asset wins outright because it's actually usable as money, while Ethereum still carries a lot of the weight behind the scenes.

Meanwhile, Tether made $1.04 billion in profit last quarter, mostly by holding dollars in US Treasuries earning 4%+ interest. That makes it one of the largest holders of US government debt on the planet.

Ethereum works the opposite way. Stake your ETH, and you get paid directly for helping secure the network, around 1.7% to 4% a year (depending on the staking platform). The demand has outpaced supply: over 3.5 million ETH is stuck in a waiting line to be staked, mostly from ETFs and companies wanting a piece of it.

4. Regulation

Verdict: Ethereum — Tether is losing ground in the EU

On July 1, 2026, MiCA's grace period expired across all 27 EU member states. Of the roughly 1,200-plus firms that once held national crypto registrations, only about 194–210 had converted to full MiCA authorization by the deadline. USDT, along with DAI, USDe, FDUSD, PYUSD, and TUSD, remains unauthorized as an EU e-money token.

It means MiCA-licensed exchanges (Coinbase, Kraken, Binance, Bitstamp, Crypto.com, and others) have been geofencing or delisting USDT trading pairs for EU users since as early as late 2024. Roughly $17.5 billion in EU-circulating USDT is directly affected.

CEO Paolo Ardoino has publicly argued that the rule's requirement to hold 60% of reserves in European bank deposits is incompatible with Tether's model. For more on Tether's thinking straight from Ardoino, here's the full interview:

This is not a ban on holding USDT in self-custody (ESMA has clarified there's no restriction there), but it is a hard wall between USDT and the regulated European exchange system.

Ethereum's regulatory arc in the same field is different. On March 17, 2026, the SEC and CFTC issued a joint interpretive release explicitly naming ETH (alongside Bitcoin, Solana, XRP, and 13 others) a "digital commodity". It's not a security and staking itself doesn't constitute a securities transaction. That guidance isn't yet codified into permanent statute, but it's already functioning as the operative rulebook.

5. Institutional Adoption

Verdict: Both are institutionally embedded in incomparable ways, but Ethereum wins as infrastructure

This category has the widest gap between headline and nuance. Ethereum has become the default settlement layer for tokenized traditional finance:

BlackRock's BUIDL fund launched on Ethereum in March 2024 with a $100 million seed. It's grown to roughly $2.5 billion in assets under management.

JPMorgan went further. It launched multiple tokenized money-market funds (MONY, then JLTXX) directly on Ethereum's public network.

The tokenized real-world asset (RWA) market passed $32 billion in 2026. Ethereum's share of that has historically run somewhere near 50%.

Tether's institutional footprint looks completely different in kind: it's not infrastructure other institutions build on, it's an institution in its own right. Tether is one of the largest sovereign-scale holders of US government debt globally (over $141 billion).

So, Ethereum wins as the substrate institutions are choosing to build on. Tether wins, if you can call it winning, as a macro-financial entity institutions increasingly have to reckon with.

6. Censorship Resistance & Control

Verdict: Ethereum — no built-in freeze mechanism

Every dollar of USDT exists because Tether Limited says it does, and Tether can make it stop existing on command. Its T3 Financial Crime Unit, a joint effort with Tron and TRM Labs, has already frozen wallets tied to illicit transactions; one disclosed batch amounted to only about 0.16% of TRC-20 supply, but the capability itself is the point.

Under the GENIUS Act, permitted stablecoin issuers are explicitly treated as financial institutions subject to the full Bank Secrecy Act. That's arguably a feature for compliance-minded institutions and a bug for anyone valuing censorship resistance: a USDT balance is only as final as Tether's compliance department allows it to be.

Ethereum, the base protocol, has no equivalent kill switch. It doesn't know what asset is moving across it; ETH itself can't be frozen by any central authority, and the network has no built-in blacklist function. Individual tokens riding on top of Ethereum, including Ethereum-based USDT, can still be frozen by their issuers. But that's an application-layer property, not a base-layer one.

For anyone whose use case genuinely requires settlement finality that no company or government can reverse, this is the one category where the two assets are opposites by design.

So, Which One Should You Actually Hold?

Treating it as a real contest is how you end up making a bad allocation decision based on a headline about a coin flip that lasted a few hours.

These are structurally different tools. Tether is a cash-equivalent, a way to hold, move, and settle dollar-denominated value without touching a bank. Ethereum is a productive, volatile, supply-elastic network asset.

If your goal is capital preservation, cross-border settlement, or parking liquidity between trades, Tether does that job. If your goal is growth exposure, yield, or a bet on decentralized infrastructure becoming Wall Street's back office, Ethereum does that job.

The flip on June 26 wasn't a signal about which asset "won." It was a symptom of where capital hides when it's scared. And a reminder that market cap, on its own, has never been a very good way to answer the question "which of these should I own."

Ethereum is about to undergo its most radical transformation since the Merge. Discover how the newly announced "Lean Ethereum" roadmap will unlock blazing-fast speeds, post-quantum security, and built-in validator privacy to rebuild the network's core architecture.